A very substantial private lending opportunity, right now

December 2021

The following was published on Livewire Markets on 2 December 2021.

In a world of low, some would say subterranean, interest rates, the CIPAM Credit Income Fund has been designed to exploit the opportunities in both public and private markets, and deliver yields around 1.5% above comparable daily liquid strategies.

CIPAM is a wholly-owned investment manager of the Challenger Group, and we’ve been investing in both public and private markets for over 15 years. Our pre-GFC experience gives our customers confidence and, with $16 billion under management, we’re one of the largest credit managers specialising in both public and private markets in Australia, including the deep and diverse Australian private lending market.

This market is worth over $3 trillion, with around $2.5 trillion of that dominated by the banking system. But while the banks have a 95% share of residential mortgage lending, they have only a 75% share of business lending. If we strip out the public bond market, we’re still left with a very substantial opportunity set of around $70 billion.

And it is this opportunity set that CIPAM targets: those areas of the market that are unattractive to the major banks because of capital regulation or other factors.

For more detail on CIPAM’s strategies in the private lending market please watch the video below.

This transcript has been edited for clarity and length

Hi, I’m Pete Robinson, Head of Investment Strategy at CIP Asset Management, which we like to refer to as CIPAM. I’m pleased to be here today to introduce you to the CIPAM Credit Income Fund.

Our history dates back to 2005, investing in both public and private markets for over 15 years. Our history has always been around liability-driven investment strategies, and that has led us to some of the less efficient parts of credit markets, and particularly that private lending market opportunity which I’ll be discussing with you today.

We have pre-GFC investment experience. And I think that gives our clients confidence and comfort in how our strategies have performed through a full credit cycle.

At $16 billion under management, we’re one of the largest credit managers specialising in both public and private markets in Australia. And our unique, independent credit risk function, which effectively acts as an in-house credit rating agency, provides a unique differentiator and comfort when we are investing in those less liquid parts of the market.

(As above) the private lending market in Australia is deep and diverse. At over $3 trillion, with around $1 trillion of business lending, it is a very substantial market opportunity set. Around $1.5 trillion of the $3 trillion is residential mortgage lending. And, of course, around $2.5 trillion of that is dominated by the banking system.

But the bank’s dominance is not equally distributed across all segments of the market.

They have a 95% share of residential mortgage lending, but only a 75% share of business lending. If we strip out the public bond market, we’re still left with a very substantial opportunity set of around $70 billion.

And it is this opportunity set that CIPAM targets, those areas of the market that are unattractive to the major banks because of capital regulation or other factors.

From the perspective of a borrower, they’re more than happy to pay the higher interest rate because, in return, they get certainty of execution, they get more tailored or flexible terms in the underlying loan, and they get speed of execution.

All of those are important non-financial factors that drive the choice of a non-bank private lender.

For private lenders, of course, there is a higher yield that’s available when you compare the yields on private markets to public markets.

But there’s also better structural protections because you’re negotiating directly with the borrower. It’s a less efficient and competitive market, and there’s diversification away from the listed market.

Now, success for a non-bank private lender is really driven by three key factors.

Number one is scale. Scale matters in private markets because borrowers want a full solution, not part of one. Experience is also important because they want to deal with someone who can provide consistent and timely feedback, which only comes with experience. Track record is also crucial in private lending markets because borrowers want to deal with someone who’s got a long history and track record of consistent behaviour through a full credit cycle, and indeed through the life of a loan.

Borrowers are willing to pay additional and higher interest rates in order to deal with a lender who has scale, experience, and track record.

We’ve mentioned the attractive diversification opportunities within the private lending market within Australia. While many of these names are not represented in public markets, they will be familiar to many of you.

I’m sure many have shopped at Harris Farms, eaten Red Rooster, or visited many of the properties that are underpinned within our commercial real estate portfolio. Some of you may have used a Zip buy now pay later loan, or borrowed from Pepper to get a mortgage.

These names are not available directly in the public markets, and, generally, are underrepresented within public market portfolios. By investing in private markets, you are able to access these unique opportunities and exposures, adding diversification within your investment portfolios.

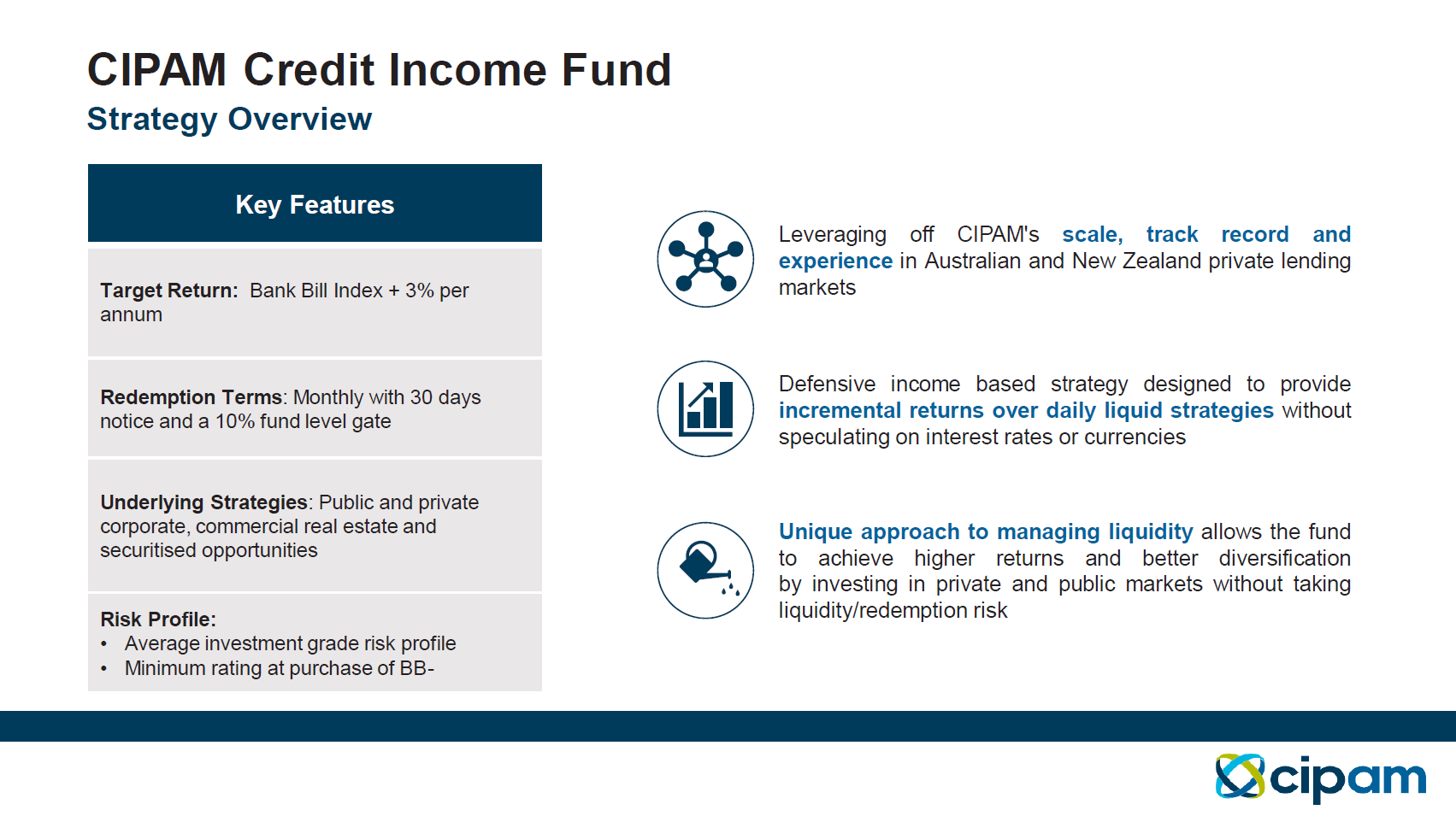

Now, let’s turn to the CIPAM Credit Income Fund. The CIPAM Credit Income Fund is a unique strategy, targeting a cash plus 3% return (net of fees) with monthly liquidity and a 10% fund level gate.

It’s designed to provide incremental returns over daily liquid strategies, whilst maintaining a comparable level of credit risk with an average investment grade rating profile.

The unique approach to managing liquidity within the strategy allows us to access those opportunities in public and private markets, which are the least efficient corners of the market, and really offer some important differentiation in today’s low spread and low-yield environment.

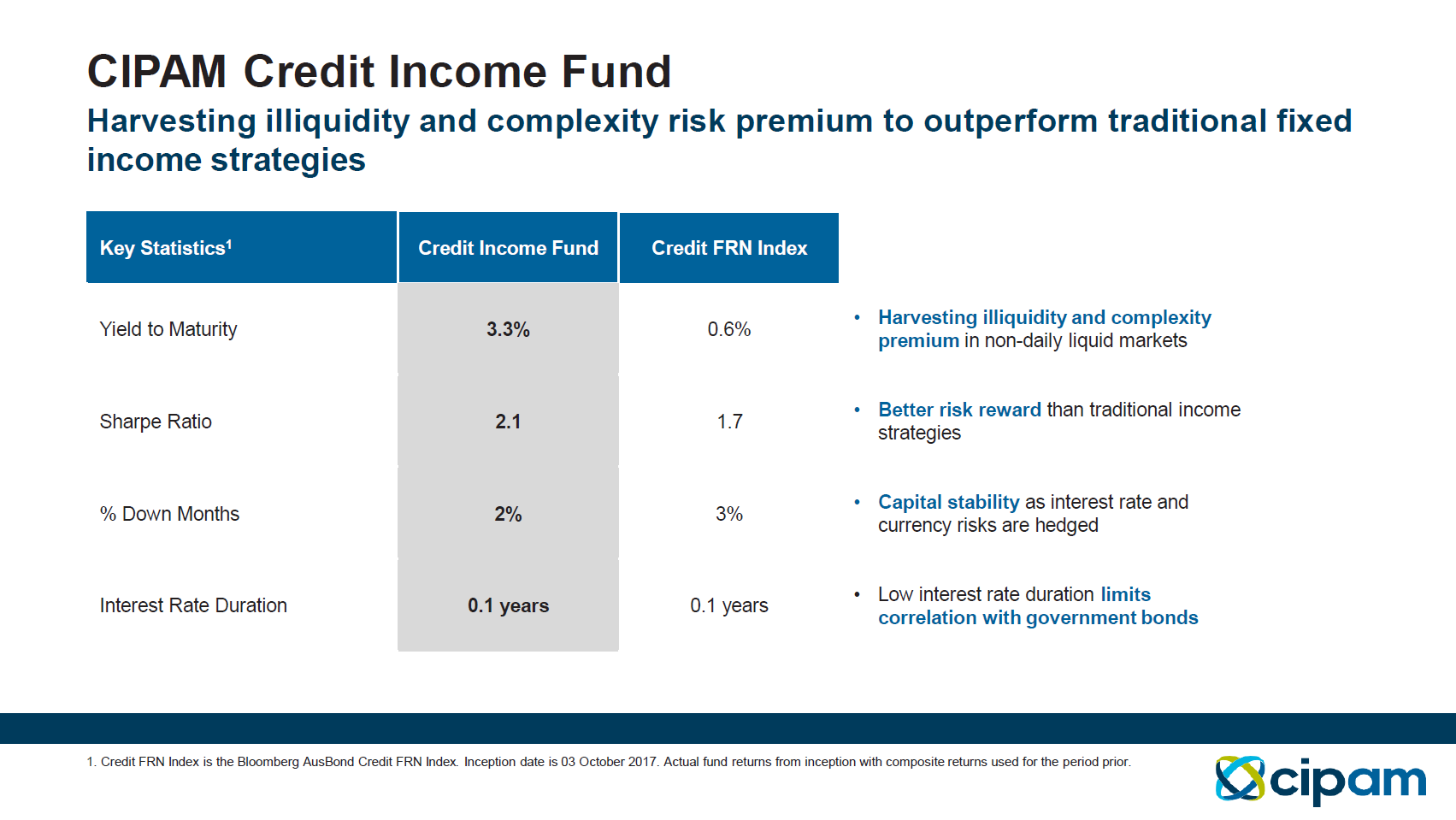

And this is demonstrated on this slide, where we show the incremental yield to maturity that can be generated through an allocation to those less liquid parts of the market, and flowing through to the better risk-reward that comes from a strategy that targets credit spread and illiquidity risk premium, rather than speculating on the more volatile interest rate or currency risks available in the market today.

Capital stability is core to our strategy, as is shown by the small number of down months since we launched the strategy in 2017. And, importantly, we have exhibited a low correlation with interest rate markets because of the fact that we do not speculate on those interest rate risks; which right now are extremely volatile.

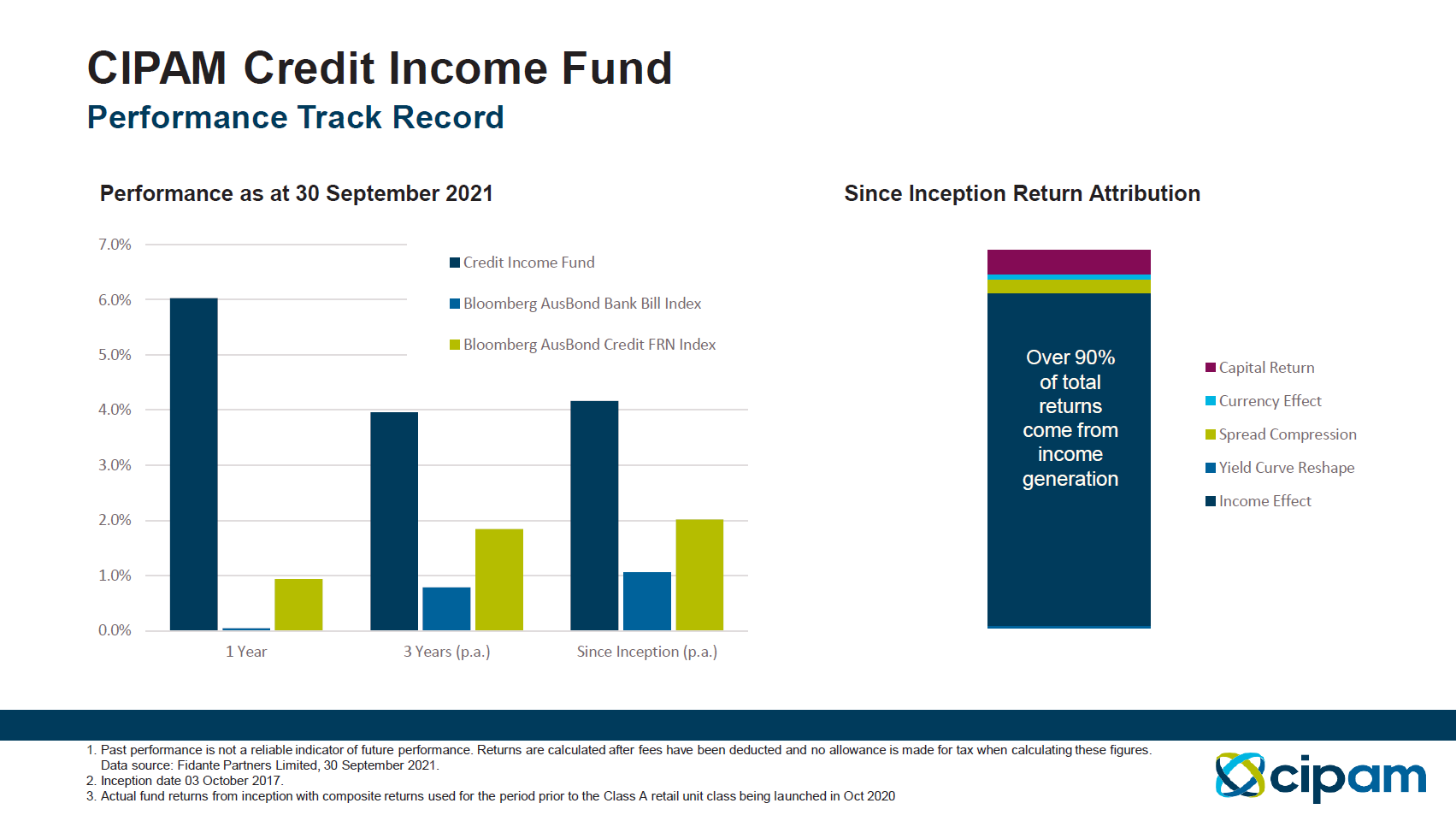

On this slide, we show the performance track record of the CIPAM Credit Income Fund. Since launching in October of 2017, we’re pleased to have provided consistently strong returns to our clients, outperforming the Bloomberg Credit FRN Index, which is a proxy for daily liquid strategies. And, even more pleasingly, have illustrated that 90% of the returns of the strategy have come from income generation, which is exactly what we target within the strategy. We don’t speculate on interest rate or currency risks, and that leads to capital stability. Essentially, within the strategy, what we’re doing is finding the right people to lend to, lending to them at the right interest rate, and getting paid back.

The portfolio positioning is really driven by the unique structure of the Credit Income Fund. By providing monthly liquidity with a 10% fund level gate, we’re not forced to hold highly liquid securities which offer little in the way of return.

We can diversify the portfolio while still maintaining a weighted average investment grade credit risk profile, but not concentrating in those overrepresented sectors within the public market, such as financial credit.

This introduces much greater diversification, both within the strategy, but also diversification away from a listed equity strategy, which is going to be represented by many of the same names in a traditional daily liquid credit fund.

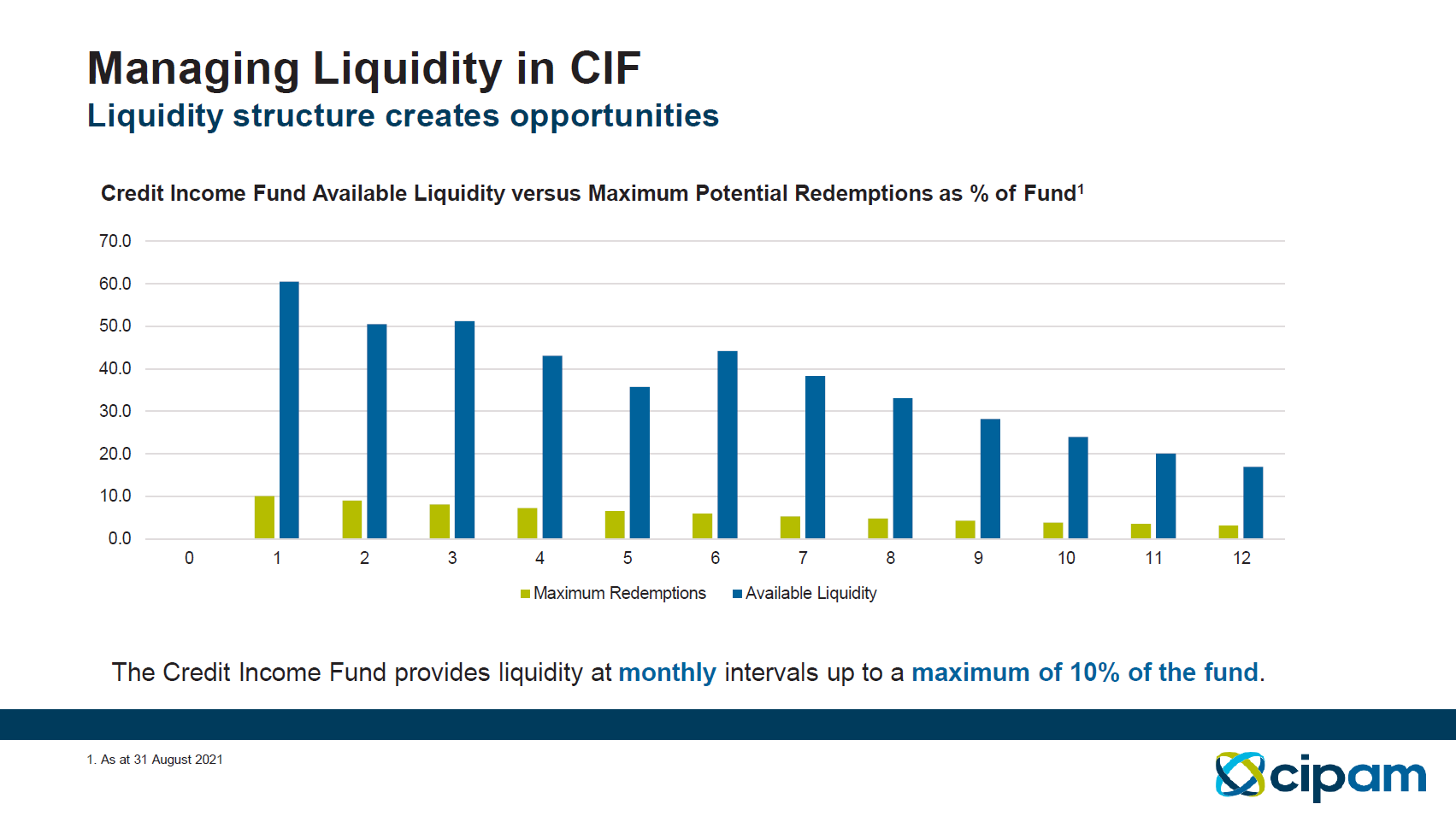

The management of liquidity within the CIPAM Credit Income Fund is a key differentiator. As I mentioned earlier, the fund offers monthly liquidity with a 10% fund level gate. And what that means is, only 10% of the funds can be redeemed in any given month. That effectively creates a liability profile for the fund, of which we can invest in those less liquid parts of the credit markets.

And what we’ve shown here on this slide is a bar chart, illustrating exactly how that redemption profile can work. As you can see, the green bars show the maximum 10% that could be redeemed from the fund in any given month. And the blue bars represent the available liquidity of the fund over that period of time.

So in month one, we have 60% of the fund in available liquid investments, versus a maximum 10% that can be redeemed from the fund.

This allows us to traverse those less liquid parts of the credit market, where those less efficient and better priced opportunities are available. And that’s what drives the excess returns generated by the strategy.

I’m pleased to have been able to introduce you to the CIPAM Credit Income Fund today. We think, in a world of uncertainty around interest rates, inflation expectations and equity valuations, the core attributes of the Credit Income Fund are especially important. Those are:

- Consistent income

- Capital preservation

- Attractive diversification.

All of which are packaged within an appropriately structured vehicle that protects investors from redemption risk, while allowing them to access these unique opportunities that exist in the less liquid and less efficient parts of the Australian credit markets.

DISCLAIMER

Unless otherwise specified, any information contained in this material is current as at date of publication and is provided by Challenger Investment Partners Limited (CIP Asset Management, CIPAM) (ABN 29 092 382 842, AFSL 234678), the investment manager of the CIPAM Credit Income Fund ARSN 620 882 055 (Fund). Fidante Partners Limited ABN 94 002 835 592, AFSL 234668 (Fidante) is the responsible entity and issuer of interests in the Fund. Fidante and CIPAM are members of the Challenger Limited group of companies (Challenger Group). Information is intended to be general only and not financial product advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider whether the information is suitable to your circumstances. The Fund Target Market Determination and Product Disclosure Statement (PDS) available at (VIEW LINK) should be considered before making a decision about whether to buy or hold units in the Fund. Past performance is not a reliable indicator of future performance.

Fidante and CIPAM are not authorised deposit-taking institutions (ADI) for the purpose of the Banking Act 1959 (Cth), and their obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante and CIPAM. Investments in the Fund are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group.

Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon.