What We’re Watching: Why everyone should care about the California wildfires

February 2025

The California wildfires of January 2025 were an extraordinary event. 29 people died, more than 200,000 people were forced to evacuate and over 18,000 homes were destroyed. Economists at UCLA estimated total property and capital losses could range between US$95 billion and US$164 billion with insured losses at up to US$75 billion making it the second most costly event after Hurricane Katrina (over US$100 billion in losses, over US$40 billion insured loss). They estimated a $4.6 billion hit to GDP with total wage losses of US$297 million for affected businesses.

But despite the size of the losses the insurance industry has sailed through the event relatively unscathed with minimal price reason at the major P&C insurers who had limited coverage in California after previous wildfires and accessed reinsurance covered to cap potential losses.

Indeed the insured losses do not provide the full picture when considering the economic impact of the California wildfires. AccuWeather has estimated that the total damage plus broader economic slowdown total between US$250 billion and US$275 billion making the wildfires the most costly natural disaster in US history, exceeding the US$200 billion total from Hurricane Katrina.

But even these figures may understate the impact of the California wildfires and the reason relates to insurance coverage and ultimately house prices.

The increased frequency and severity of extreme weather events is making insurance, a must have to obtain a mortgage, either extremely expensive or in some cases unavailable. Where insurance is unavailable, the government has had to step in as the insurer of last resort.

As the wildfires were still ravaging parts of California the US Department of the Treasury’s Federal Insurance Office (FIO) released a report which highlighted how homeowners insurance has increased 8.7% faster than the rate of inflation from 2018-2022. Some areas experienced doubling of insurance premiums over the period. This in turn led to much higher policy non-renewal rates meaning more properties were effectively uninsured.

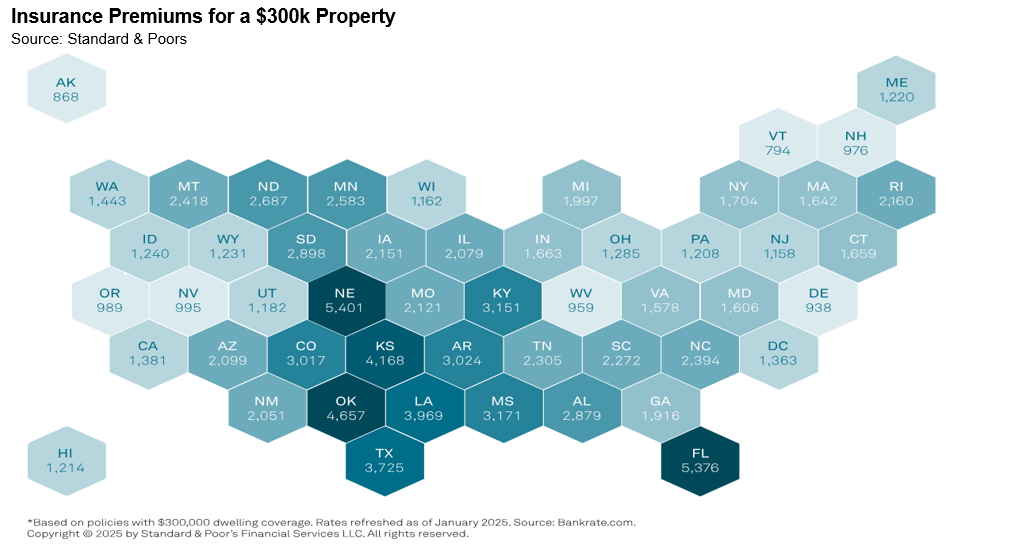

Prior to the wildfires property insurance in California was not expensive relative to other states but looks likely to increase sharply. In other parts of the United States homeowners are paying over 1.5% of their property value per annum in insurance premiums versus less than 0.5% in California. California’s total housing stock is worth US$10 trillion, equivalent to one fifth of total housing stock in the United States. In 2024 S&P estimated that if insurance premiums increased by 20% annually versus 10% annually the implied impact on houses prices at a 4% discount rate would be around 10%.[1] Consider that in California State Farm, the state’s largest insurance has requested a 22% average increase to insurance premiums having filed for a 30% rate increase in mid 2024.

At a more micro level residents in Laytonville, California saw insurance premiums increase by 106% over the 2018-22 period with an average premium of $3,257 in 2022 (which we estimate would be closer to US$6,000 today). In 2024, Zillow quotes the average house price in Laytonville at $344,853, having declined by over 10% over the past 12 months (compared to a national average of around 5% year on year growth). This means a resident in Laytonville California will be paying north close to 2% of the property value in home insurance up from less than 0.5% in 2018. From the perspective of an investor this is like saying that the net yield on a property has declined by 1.5% which on a cap rate basis is equivalent to around a 20% reduction in implied value.

Adding to the risk on house prices are those properties where insurers refuse to provide coverage. Between 2020 and 2022 insurers declined to renew 2.8 million homeowner policies. Estimates suggest that 10% of homes in Los Angeles are uninsured. There are government programs to provide cover where private insurance refuses but these cap coverage at $3 million and come with premiums that are double private insurance costs. The California state government has also introduced legislation requiring insurers to have at least 85% of their statewide portfolio in risk areas which will result in further premium increases and inevitably even larger hits to house prices.

Add further to this that these back of the envelope numbers do not include the impact of other insurance premium increases such as auto insurance and business insurance, all of which have risen by as much if not more than home insurance. Plus the fact that the costs of rebuilding a house will skyrocket.

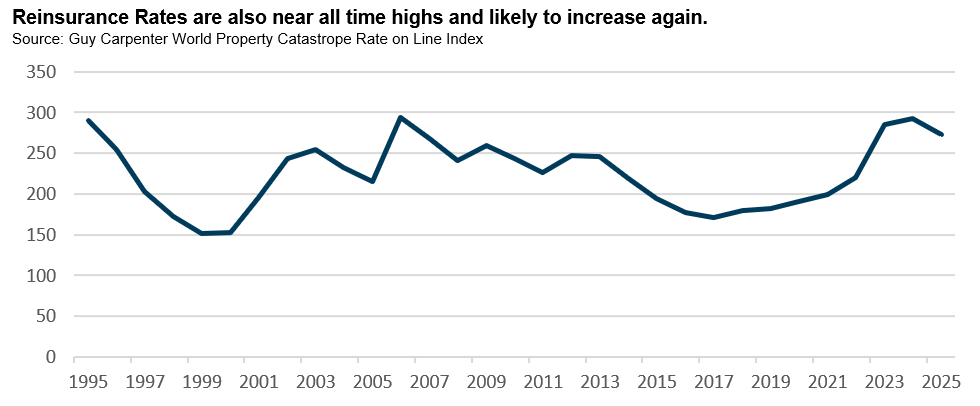

Having increased almost 70% since the lows in 2017 before levelling off in the 1 January 2025 renewals reinsurance rates will also likely increase as demand for reinsurance will increase but capacity will be limited. This further increases the likelihood of increases in the cost of primary insurance even to those not in California.

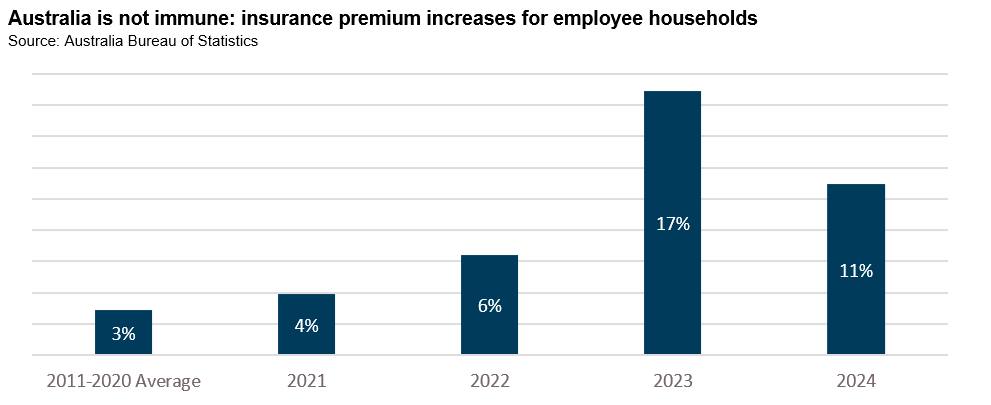

But before you thank your lucky stars you live in Australia and not California, consider that in Australia, employee households have seen their gross insurance costs increase by 50% from the end of 2017.

According to the Insurance Council of Australia around 1 in 12 properties (equivalent to 1.2 million properties) have some level of flood risk with around 1 in 60 at risk of flooding every 20 years. Around 1 in 3 properties (5.6 million properties) are at risk of a bushfire.

In November 2024 researchers from the University of Technology Sydney published research showing that houses in an area with a greater than a 1 in 100 year flood risk were priced a 10.8% discount. The researchers found that the cost of insurance almost was around 0.5% per annum higher for houses in a 1 in 100 year flood zone.

But perhaps the most important finding was that there was no discernible price impact where the property is located in an area with a 1 in 1000 year flood risk nor is there an impact on house prices when an area is upgraded from a 1 in 1000 year flood risk zone to a 1 in 500 year flood risk zone. This means homeowners are exposed to the risk of sharp increases in insurance premiums if climate change results in a re-categorisation of the flood risk of an area.

In many respects, Australia is even more exposed to the risk of weather events impacting house prices than even California.

- Houses are more expensive in Australia relative to incomes;

- Property yields are lower in Australia meaning small changes in running costs make large differences to property prices; and

- Australians have more mortgage debt which means property insurance is not optional.

Property investors need to consider how insurance premiums may increase through time, reducing net returns. Property lenders need to consider how increased cost of insurance could lead to higher cancellation rates leaving lenders fully exposed in the event of a weather related catastrophe. Ultimately both investors and lenders need to start considering the risk that insurance premium become a more relevant factor in the determination of house prices. By the time the flood or fire comes, it will be too late.

[1] April, 2024; The Impact of Rising Insurance Premiums on U.S. House Prices.

On behalf of the team, thanks for reading.

Pete Robinson

Head of Investment Strategy – Fixed Income | +61 2 9994 7080 | probinson@challenger.com.au

For further information, please contact:

Linda Mead | Senior Institutional Business Development Manager | T +61 2 9994 7867 | M +61 417 675 289 | lmead@challenger.com.au | www.challengerim.com.au

Disclaimer: The information contained in this publication has been prepared solely for solely for the addressee. The information has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this report, whether express or implied, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Fidante Partners Limited ABN 94 002 895 592 AFSL 234 668 (Fidante Partners) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, Fidante Partners or any director, officer, employee or agent of Fidante Partners, do not accept any liability (whether in negligence or otherwise) for any errors or omissions contained in this report.